Note

Go to the end to download the full example code. or to run this example in your browser via JupyterLite or Binder

Handling Incomplete Datasets: Inception, Expiry, and Default#

When working with large datasets over long timeframes, we commonly encounter:

Inception: Assets that began trading after the start of the dataset.

Expiry: Expiring assets such as bonds, options, and futures.

Default: Assets that defaulted.

Voluntary Delisting

These events create challenges for portfolio optimization and backtesting. A common workaround is to focus only on assets with complete datasets, excluding those with later inception dates, defaults, or earlier expirations. However, this approach either shortens the backtesting period or reduces the number of assets, potentially introducing survivorship bias.

An additional challenge arises with assets that have known expiration dates (e.g., options, bonds, futures). If an asset is due to expire in the next period, it may be preferable to exit early, especially if it’s not cash-settled.

In this tutorial, we will demonstrate how to implement all these rules in a single

Pipeline that can be used with cross-validation techniques such as WalkForward and

hyperparameter tuning tools like GridSearchCV.

Data#

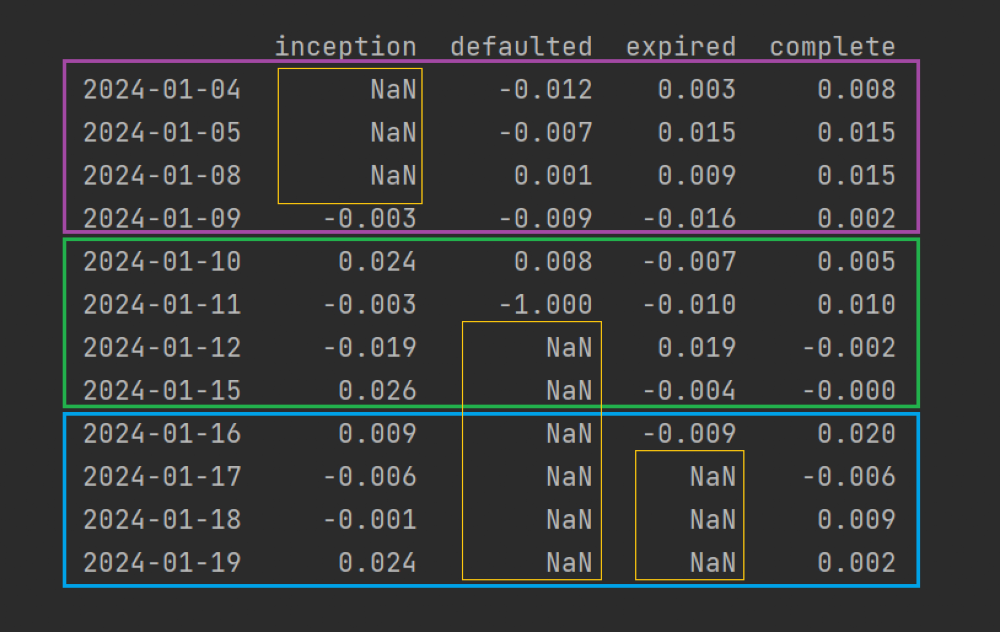

Let’s create price data for four hypothetical assets over 13 days:

inception: Asset with a later inception date.defaulted: Asset that defaulted.expired: Asset that expired.complete: Asset with a complete price history.

We’ll convert these prices to returns and split the dataset into 3 rebalancing periods of 4 days each.

import datetime as dt

import matplotlib.image as mpi

import matplotlib.pyplot as plt

import numpy as np

import pandas as pd

from sklearn import set_config

from sklearn.impute import SimpleImputer

from sklearn.model_selection import GridSearchCV

from sklearn.pipeline import Pipeline

from skfolio.model_selection import WalkForward, cross_val_predict

from skfolio.optimization import EqualWeighted

from skfolio.pre_selection import SelectComplete, SelectNonExpiring

from skfolio.preprocessing import prices_to_returns

def generate_prices(n: int) -> list[float]:

# Just for example purposes

return list(100 * np.cumprod(1 + np.random.normal(0, 0.01, n)))

prices = pd.DataFrame(

{

"inception": [np.nan] * 3 + generate_prices(10),

"defaulted": generate_prices(6) + [0.0] + [np.nan] * 6,

"expired": generate_prices(10) + [np.nan] * 3,

"complete": generate_prices(13),

},

index=pd.date_range(start="2024-01-03", end="2024-01-19", freq="B"),

)

X = prices_to_returns(prices, drop_inceptions_nan=False, fill_nan=False)

img = mpi.imread("../images/incomplete_dataset.png")

fig, ax = plt.subplots(figsize=(10, 6.327))

ax.imshow(img)

ax.axis("off")

plt.subplots_adjust(left=0, right=1, top=1, bottom=0)

Pipeline#

Our Pipeline will handle the following cases:

When we train our optimization model on the first period (magenta box), we want to exclude the “inception” asset.

When testing on the second period (green box), we want to capture the loss on the “defaulted” asset (the -100% on 2024-01-11) without failing on the subsequent NaNs.

Then, when we train on the second period, we want to include the “inception” asset, exclude the defaulted asset, and also exclude the “expired” asset that will expire in the next test period (blue box).

set_config(transform_output="pandas")

model = Pipeline(

[

("select_complete_assets", SelectComplete()),

(

"select_non_expiring_assets",

SelectNonExpiring(

expiration_dates={"expired": dt.datetime(2024, 1, 16)},

expiration_lookahead=pd.offsets.BusinessDay(4),

),

),

("zero_imputation", SimpleImputer(strategy="constant", fill_value=0)),

("optimization", EqualWeighted()),

]

)

The transformer SelectComplete handles the “inception” and “defaulted” assets,

while SelectNonExpiring excludes assets close to expiration.

SimpleImputer replaces NaNs with 0s on the “defaulted” asset in the test period.

Walk-Forward Cross-Validation#

Now, we pass this pipeline model into cross_val_predict using WalkForward:

pred = cross_val_predict(model, X, cv=WalkForward(train_size=4, test_size=4))

As expected, the pipeline correctly applies our rules to each period:

df = pred.composition

df.columns = ["Period 2 (green)", "Period 3 (blue)"]

df

And from the out-of-sample returns, we can see that the default event was captured on 2024-01-11:

df = pred.returns_df

df

2024-01-10 -0.003283

2024-01-11 -0.332897

2024-01-12 0.007035

2024-01-15 -0.001003

2024-01-16 -0.006270

2024-01-17 0.002679

2024-01-18 -0.001381

2024-01-19 -0.005838

Name: returns, dtype: float64

Step-by-Step Fitting with WalkForward#

Let’s break down the cross_val_predict by calling fit and predict on each

period:

print("Rebalancing Period 1")

model.fit(X.iloc[:4])

portfolio = model.predict(X.iloc[4:8])

print(portfolio.composition)

print(portfolio.returns)

print("Rebalancing Period 2")

model.fit(X.iloc[4:8])

portfolio = model.predict(X.iloc[8:])

print(portfolio.composition)

print(portfolio.returns)

Rebalancing Period 1

EqualWeighted

asset

defaulted 0.333333

expired 0.333333

complete 0.333333

[-0.00328326 -0.33289689 0.00703457 -0.00100265]

Rebalancing Period 2

EqualWeighted

asset

inception 0.5

complete 0.5

[-0.00627032 0.00267862 -0.00138139 -0.00583791]

Hyper-Parameter Tuning#

The Pipeline model can also be passed to GridSearchCV to find the optimal

hyperparameters for a specified score (by default, the out-of-sample average

Sharpe ratio). For example, we could use it to find the optimal exit time before a

bond expires:

grid_search = GridSearchCV(

estimator=model,

cv=WalkForward(train_size=4, test_size=4),

param_grid={

"select_non_expiring_assets__expiration_lookahead": [

pd.offsets.BusinessDay(i) for i in range(20)

],

},

)

grid_search.fit(X)

model = grid_search.best_estimator_

Total running time of the script: (0 minutes 0.480 seconds)